Customer service was a $400 billion industry in 2023. By the end of 2025, the first wave of AI agents is resolving complaints, negotiating refunds, and navigating phone trees without a human in the loop.

Every industry that has undergone deep technological disruption shows the same seven signals before the collapse becomes obvious. You can see them in how electricity ate the steam-power industry, how cloud computing ate on-premise IT, how GPS ate the cartography business. The signals appear in sequence, usually over three to seven years, and by the time most incumbents notice all seven, it is too late to reposition.

AI is running this pattern faster than any previous technology. The signals that took a decade to appear in cloud computing are appearing in agent commerce in 18 to 24 months. Here is how to read them.

Why Domains Collapse in Patterns

A domain collapses when the core cognitive task that justified its economic structure becomes cheap enough to be routine. Accounting collapsed when spreadsheets made arithmetic free. Travel agencies collapsed when search made itinerary research free. The collapse is about which tasks the technology makes so cheap that the old pricing structure becomes absurd.

The SolveEverything framework describes this as a four-stage process: making invisible signals legible, building repeatable procedures, institutionalizing those procedures into markets, and finally demonetizing the capability entirely. Each stage produces observable signatures. If you know what to look for, you can place any industry on the curve and estimate how far it has to fall.

Agent commerce is currently between stages two and three. The signatures are appearing in real time. Here they are.

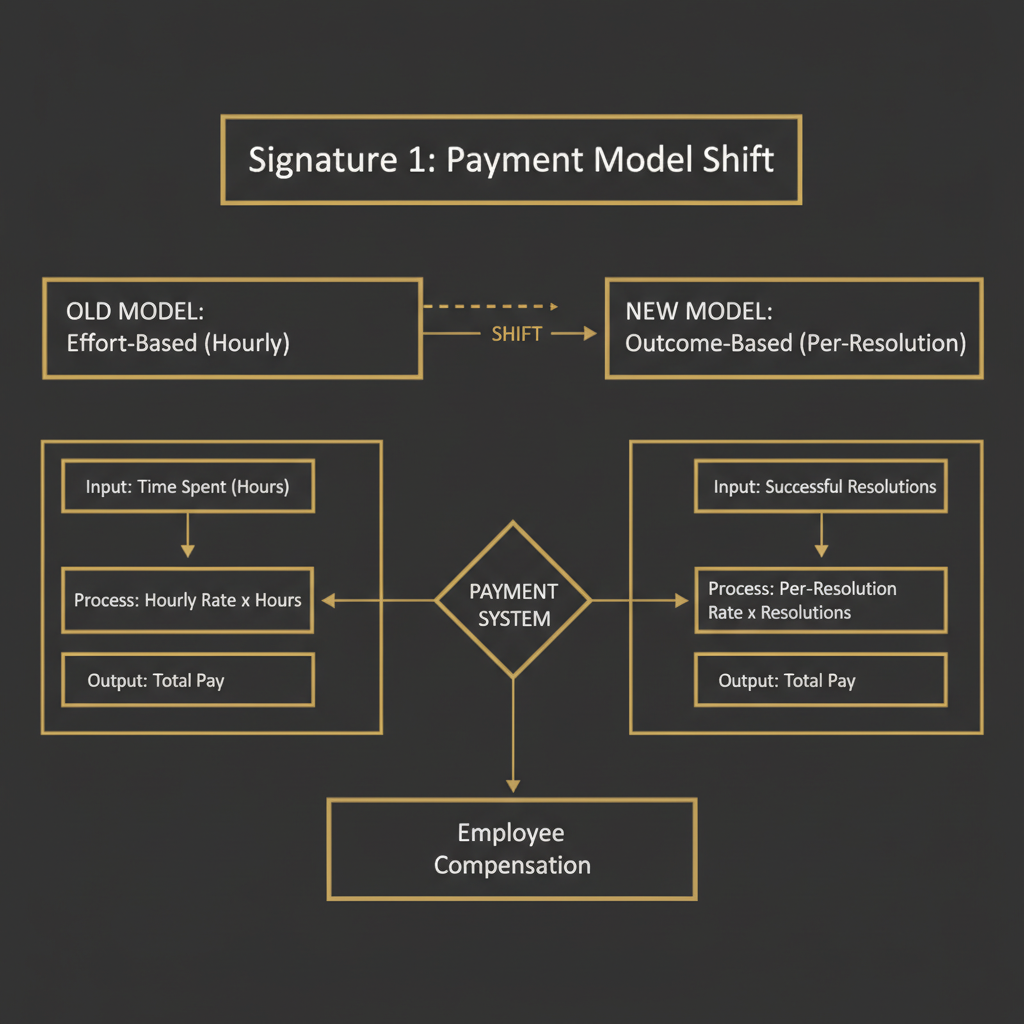

Signature 1: Payment Shifts from Effort to Outcome

The oldest pricing signal in any domain collapse is when buyers stop paying for time and start paying for results. Lawyers charged by the hour because legal judgment was opaque. Consultants charged by the day because their process was the product. The moment a domain becomes measurable enough to price by outcome, the effort-based pricing model is on borrowed time.

In customer service AI, this is already happening. Freebot charges nothing until it wins your dispute. Freway charges nothing until it recovers an abandoned checkout. OneShot's pricing is per-tool-call, not per-seat or per-hour. The economic logic is the same in all three cases: the task is measurable, so you can price the measurement.

When you see a market where the leading new entrants all charge on outcomes and the incumbents still charge on effort, the incumbents have roughly 18 months before they face serious pricing pressure. The outcome-based players are subsidizing discovery now. They will raise prices once they own the benchmark.

Signature 2: Documents Become Machine-Verifiable Proofs

The second signature is epistemic. In immature domains, knowledge lives in documents: reports, summaries, assessments, opinions. These require human interpretation. In collapsing domains, documents get replaced by structured proofs that machines can verify without interpretation.

Consider the difference between a credit report and a real-time bank feed. A credit report is a document, produced by humans, interpreted by loan officers, with a lag of weeks. A bank feed is a proof: machine-readable, real-time, cryptographically attributable. The mortgage industry is slowly collapsing around this distinction.

In agent commerce, the equivalent shift is from conversation logs to transaction receipts. When an AI agent makes a phone call, sends an email, or verifies an identity, the output needs to be a proof, not a summary. The x402 protocol is an early example of this: it lets agents pay for tools with USDC in a way that is cryptographically verifiable, not just logged. A receipt that a machine can read is worth more than a report that a human has to interpret, because it can be composed into other proofs without human intervention.

Watch for this signature in any domain where audit trails are currently produced as PDFs.

Signature 3: Discrete Projects Become Continuous Pipelines

The third signature is temporal. Pre-collapse industries sell discrete engagements: the audit, the campaign, the assessment, the report. Post-collapse industries run continuous pipelines. The work does not stop between engagements because the pipeline is always watching for the next trigger.

Marketing agencies sold campaigns. Marketing automation platforms sold always-on pipelines. The campaign model collapsed in email marketing around 2012. It is collapsing in paid social now. The agencies that survived are the ones that rebuilt around pipeline management rather than campaign production.

In agent commerce, the equivalent is the shift from "run this agent task" to "this agent is always running." Freway's Janine does not wait for a merchant to start a campaign. She watches every checkout session in real time and intervenes at the moment hesitation appears. The trigger is continuous, the response is automated, and the merchant never has to initiate a project. This is what a pipeline looks like in agent commerce, and it is structurally incompatible with project-based agency pricing.

Signature 4: Individual Heroics Yield to Systems Engineering

The fourth signature is organizational. Every pre-collapse domain has a mythology of the exceptional individual: the 10x engineer, the rainmaker partner, the star analyst. This mythology is not entirely wrong. In domains where the core task is not yet systematized, individual judgment genuinely drives outcomes. But the mythology becomes economically dangerous once the task becomes automatable, because it causes organizations to optimize for hiring the exceptional individual rather than building the system that makes average individuals exceptional.

Google did not beat AltaVista because Google had better engineers. It beat AltaVista because PageRank was a system that turned the entire web into a signal, while AltaVista relied on human editors to curate quality. The system beat the heroics.

In agent commerce, the equivalent is the shift from "we have a great sales rep" to "we have an orchestration layer that makes every touchpoint as good as our best rep's best day." Freway's architecture is a useful example: the agent handles six channels simultaneously, in real time, without fatigue or variance. No human rep can do that. The question is not whether the agent is as good as the best human. The question is whether the system produces better aggregate outcomes than a team of humans, and for most Shopify merchants, the answer is yes at a fraction of the cost.

Signature 5: Proprietary Secrecy Gives Way to Ecosystem Transparency

The fifth signature is about information strategy. In immature domains, competitive advantage comes from proprietary knowledge: the secret sauce, the undisclosed methodology, the black-box model. In collapsing domains, this strategy inverts. The winners publish their benchmarks, open their protocols, and compete on execution rather than on secrecy.

This happened in cloud infrastructure. Amazon could have kept S3's architecture secret. Instead, they published the API, built an ecosystem around it, and made switching costs structural rather than informational. The open API became the moat, not the closed architecture.

In agent commerce, Soul.Markets is betting on this inversion. The marketplace publishes agent identities as public soul.md files, making capabilities machine-readable and discoverable. The bet is that ecosystem transparency compounds faster than proprietary secrecy. When any agent can discover and hire any other agent through a public protocol, the network effects dwarf what any single closed system can build. The domains that are currently most secretive about their AI methodologies are the ones most vulnerable to this inversion.

Signature 6: Average-Case Optimization Shifts to Tail-Risk

The sixth signature is statistical. Pre-collapse industries optimize for the median case. Post-collapse industries optimize for the tail. This sounds abstract, but the practical consequences are large.

Insurance pricing before actuarial science optimized for what most claims looked like. After actuarial science, it optimized for the distribution of all claims, including rare catastrophic ones. The companies that kept optimizing for the median went bankrupt when the tail showed up. The companies that modeled the tail correctly priced it into the product and survived.

In agent commerce, the equivalent is the shift from "how do we handle the typical customer service call" to "how do we handle the customer who has been on hold for three hours, is furious, and will post about it publicly if we fail." Freebot is explicitly a tail-risk product: it exists for the cases where the normal customer service channel has already failed. The agent's job is to handle the worst cases, not the median cases. Any AI system that is only tested on average-case inputs will fail in production, because production is full of tail cases that the average-case model has never seen.

A useful heuristic: if an AI system's demo always shows a clean, cooperative scenario, it is optimized for the median. Ask what happens when the phone tree does not have the option the agent expects. Ask what happens when the customer service rep goes off-script. The answer tells you whether the system is ready for real deployment.

Signature 7: Talent Hoarding Becomes Compute Liquidity

The seventh signature is the one that makes executives most uncomfortable. In pre-collapse industries, competitive advantage accumulates in people. You hire the best engineers, the best analysts, the best researchers, and you pay to retain them. The talent is the moat.

In post-collapse industries, the moat is compute allocation, not headcount. The question is not "do we have the right people" but "do we have the right infrastructure to direct compute at the right problems at the right time." This is not a comfortable idea for organizations that have built their identity around talent acquisition.

The numbers make the argument concrete. A senior software engineer costs $200,000 to $350,000 per year in total compensation, can context-switch between roughly three to five projects at once, and works 40 to 50 hours per week. An agent running on OneShot costs fractions of a cent per tool call, runs 24 hours a day, and can handle thousands of parallel tasks. The comparison is not "agent vs. engineer" on a single task. The comparison is "what can you build with $350,000 in engineering salary vs. $350,000 in compute budget." For a growing class of tasks, the compute budget produces more output.

This does not mean engineers become irrelevant. It means the scarce resource shifts from engineering hours to systems design judgment. The engineers who understand this shift and reorient toward orchestration and infrastructure will be more valuable. The engineers who do not will find their compensation under pressure from below.

Reading the Signals Together

Each signature is useful on its own. Together, they form a diagnostic. Here is a quick scoring exercise: take any industry you are thinking about and count how many of the seven signatures are already visible.

- 0 to 2 signatures: the domain is in early legibility. The disruption is years away.

- 3 to 4 signatures: the domain is in active transition. Early movers are establishing positions. This is the window for infrastructure investment.

- 5 to 6 signatures: the domain is collapsing. Incumbents are losing pricing power. The question is who captures the new structure, not whether the old structure survives.

- 7 signatures: the domain has collapsed. Compete on execution, not on positioning.

Customer service scores 6 out of 7 right now. The only signature not yet fully visible is ecosystem transparency: most enterprise customer service AI is still proprietary and closed. That is the next shoe to drop, and when it does, the companies that built on open protocols will have a structural advantage over the ones that built on closed stacks.

Legal services scores 3 out of 7. Payment is still effort-based for most work. Documents are still documents. But the pipeline and systems engineering signatures are appearing in contract review and discovery. Watch the payment signature: the first legal AI that successfully prices by outcome on a high-stakes matter will be the signal that the collapse is accelerating.

Healthcare scores 2 out of 7, but the legibility work is nearly complete. Once patient data is genuinely machine-readable at scale, the other signatures will appear faster than most healthcare executives expect.

The 18-Month Window

The practical implication of this framework is about timing. Domain collapse is not instantaneous, but the window for infrastructure positioning is short. Once five or more signatures are visible in a domain, the standards and benchmarks that will govern the post-collapse structure are being set. Whoever builds the scoring system, the protocol, the marketplace, gets structural advantages that are very hard to dislodge later.

In agent commerce, that window is open right now. The OneShot SDK and the Soul.Markets protocol are infrastructure bets on the post-collapse structure of agent commerce. The bet is that outcome-based payment, machine-verifiable proofs, and ecosystem transparency will be the three load-bearing walls of the new structure, and that whoever builds the best foundation on those three walls will be very difficult to displace in 2027 and beyond.

By Q2 2027, at least one Fortune 500 company will publicly report that it replaced a headcount-based customer service operation with an agent-based system priced entirely on outcomes, and will report the unit economics as favorable. When that case study publishes, the legal and healthcare scoring exercises above will each gain two more signatures overnight. The pattern does not wait for permission.